FDA’s AI Drug Development Guidelines and What’s Next for Biopharma M&A

Also: One-Third of Pharma Molecules Now Come from China, Weekly Highlights...

Hi! This is BiopharmaTrend’s weekly newsletter, Where Tech Meets Bio, where we explore technologies, breakthroughs, and the great companies driving the biopharma and medtech industries forward.

If this newsletter is in your inbox, it’s because you subscribed or someone thought you might enjoy it. In either case, you can subscribe directly by clicking this button:

Let’s get to this week’s topics.

Brief Insights

📈 Johnson & Johnson is acquiring Intra-Cellular Therapies for $14.6 billion in the largest biotech M&A deal since 2023, announced during J.P. Morgan Healthcare Conference. J&J secures Caplyta (lumateperone), approved for schizophrenia and bipolar disorder with annual sales of ~$700M, projected to grow to $5B per year with expanded indications in depression.

💰 Denmark-based Orbis Medicines, backed by Novo Holdings and Eli Lilly, raises €90M to develop oral macrocycle drugs as alternatives to injectable biologics, leveraging its AI-driven nGen platform.

🔬 Calico's eIF2B activator fosigotifator fails to meet primary endpoints in a Phase 2/3 ALS trial, showing no significant impact on disease progression, though exploratory data hints at potential benefits with higher doses; further research is needed to assess its viability.

🔬 Recursion Pharmaceuticals advances REC-3565, a selective MALT1 inhibitor for B-cell malignancies, and REC-4539, a brain-penetrant LSD1 inhibitor for small-cell lung cancer, into clinical trials.

🔬 Insilico Medicine advances its oncology efforts with two milestones: licensing a second AI-discovered cancer drug to Menarini Group in a deal worth up to $550M, and reporting positive Phase I results for ISM5411, a gut-restricted PHD1/2 inhibitor for inflammatory bowel disease.

🔬 Novo Nordisk expands its AI-driven collaboration with Valo Health to include up to 20 cardiometabolic drug programs targeting obesity, type 2 diabetes, and cardiovascular disease, with $190M upfront and up to $4.6B in potential milestones, leveraging Valo’s Opal platform for predictive drug discovery.

🔬 Tempus partners with Genialis to develop RNA-based biomarker algorithms, combining Tempus' multimodal patient data with Genialis' Supermodel to improve cancer diagnostics, patient stratification, and optimize precision oncology therapies.

💰 PostEra expands its $610M collaboration with Pfizer to include AI-driven Antibody-Drug Conjugate (ADC) development, leveraging its Proton platform to optimize ADC payloads while advancing additional small molecule programs through their AI Lab initiative.

🔬 Profluent Bio unveils Protein2PAM, an AI model trained on 45,000 CRISPR-Cas datasets, enabling customized PAM recognition to expand CRISPR's targeting range, with potential to revolutionize gene-editing applications in research and therapy.

🔬 Neumora's kappa opioid receptor antagonist navacaprant fails to show efficacy in the Phase 3 KOASTAL-1 trial for major depressive disorder, with no significant improvement over placebo, raising concerns about the drug’s future and broader challenges in neuropsychiatric drug development.

🔬 Merck KGaA adopts Quris-AI’s organ-on-chip Bio-AI platform for preclinical drug safety testing, leveraging its AI-driven models to predict liver and kidney toxicity with high accuracy, reducing reliance on traditional animal testing.

🔬 CCM Biosciences discovers first-in-class compounds targeting SIRT3, a mitochondrial enzyme tied to aging and energy production, using AI-driven simulations to optimize activity under NAD+ depletion, clinical trials set for 2025.

🔬 Eli Lilly partners with Alchemab Therapeutics to develop up to 5 ALS-targeting antibodies, leveraging Alchemab's platform that identifies naturally occurring protective antibodies from resilient individuals.

🚀 Verdiva Bio launches with $411M in Series A funding to develop a weekly-dosed oral GLP-1 receptor agonist for obesity and cardiometabolic disorders, alongside amylin agonist programs, aiming to build a robust independent pipeline.

🔬 Sana Biotechnology reports promising first-in-human results for hypoimmune-engineered islet cell transplants in type 1 diabetes, demonstrating graft survival, insulin secretion, and immune evasion without immunosuppressive drugs.

🔬 Merck partners with Atropos Health to accelerate real-world data generation using Atropos' tools and its federated patient data network, enabling rapid analytics and publication-ready insights to support life-saving treatments.

🔬 Bayer's BlueRock Therapeutics advances bemdaneprocel, a pluripotent stem cell-derived dopaminergic neuron therapy for Parkinson’s disease, into a Phase III trial (exPDite-2), aiming to restore neural function and improve motor symptoms, enrollment starting in H1 2025.

💰 Gilead Sciences partners with LEO Pharma in an up to $1.7B deal to develop oral and topical STAT6 inhibitors for inflammatory diseases like eczema, asthma, and COPD, marking Gilead's expansion into inflammation therapeutics.

💰 Truveta raises $320M for the Truveta Genome Project to sequence up to 10M exomes, integrating genetic data with de-identified medical records to support diverse drug discovery, personalized medicine, and efficient clinical trials, in partnership with Regeneron, Illumina, and 17 U.S. health systems.

💰 AbbVie partners with Simcere on SIM0500, a trispecific T-cell engager targeting GPRC5D, BCMA, and CD3 for relapsed or refractory multiple myeloma, in a deal worth up to $1.05B.

🔬 AbbVie also faces a $3.5B impairment charge after the failure of Cerevel’s emraclidine in Phase 2 schizophrenia trials, following its $8.7B acquisition of Cerevel in late 2023.

💰 Normunity raises $75M in Series B to advance its lead T cell engager, NRM-823, into a Phase 1 trial in late 2025 and develop additional therapies targeting tumor-specific immune suppression.

💰 Boehringer Ingelheim licenses Synaffix's ADC platform technology in a deal worth up to $1.3B in milestones and royalties, expanding its oncology portfolio via NBE Therapeutics to develop next-generation antibody-drug conjugates targeting novel tumor markers.

💰 Araris Biotech partners with Chugai Pharmaceutical in a $780M deal to develop next-generation ADCs using its AraLinQ platform, enabling efficient one-step conjugation of multi-payloads to native antibodies, with Chugai funding research and retaining global commercialization rights.

💰 Sanofi partners with Alloy Therapeutics in a $400M+ deal to develop a CNS-targeted antisense drug using Alloy’s platform, designed to enhance potency and enable delivery across the blood-brain barrier, in a renewed focus on antisense R&D.

🚀 Tenvie Therapeutics launches with $200M in funding to advance a pipeline of brain-penetrant and peripherally restricted small molecules targeting neurological, cardiometabolic, and ophthalmic diseases, including IND-ready NLRP3 and SARM1 inhibitors.

This newsletter reaches over 7.7K industry leaders from organizations like NVIDIA, Microsoft, Novo Nordisk, Pfizer, Novartis, FDA, the US Department of State, Illumina Ventures, and hundreds more.

Interested in sponsoring?

Contact us at info@biopharmatrend.com

FDA Drafts Guidance for AI in Drug Development

The U.S. Food and Drug Administration has issued draft guidance providing recommendations for the use of artificial intelligence (AI) in supporting regulatory decisions about the safety, effectiveness, or quality of drugs and biologics.

This marks the agency’s first guidance specifically addressing AI's role in the development of these products.

Again, as it’s yet just a draft—it is not for implementation and contains non-binding recommendations.

Here’s what’s worth knowing:

A practical framework for AI credibility: The draft lays out a seven-step process to evaluate AI models, starting with defining the problem they’re meant to solve, understanding their context of use (COU), and identifying potential risks. High-risk applications—like those directly influencing patient safety—are subject to stricter assessments.

Keep it reliable over time: AI models aren’t a “set it and forget it” deal. The guidance underscores the need for lifecycle maintenance to address evolving data inputs, potential biases, and changes in deployment environments that could impact performance.

Get the FDA involved early: The FDA is making it clear—don’t wait until you’re ready to submit your AI-driven application. Engaging with the agency early helps clarify expectations, smooth out challenges, and build a stronger credibility plan.

Built on real-world experience: Since 2016, the FDA has reviewed over 500 AI-related submissions—this guidance reflects lessons learned from those reviews and incorporates public input from workshops, academics, and industry players.

Transparency is key: Developers need to provide detailed documentation on their AI models, from training data to evaluation metrics. The aim is to tackle issues like bias, reproducibility, and reliability head-on.

What it covers (and doesn’t): The focus is on AI used for generating data or insights that directly impact regulatory decisions. Operational uses—like streamlining internal workflows or drafting documents—and drug discovery applications are outside the scope.

The FDA wants feedback on this draft and is welcoming public comments for the next 90 days. It’s a good opportunity for developers, sponsors, and others to weigh in on how AI should be regulated in the drug development space.

The full draft guidance is available on the FDA’s website.

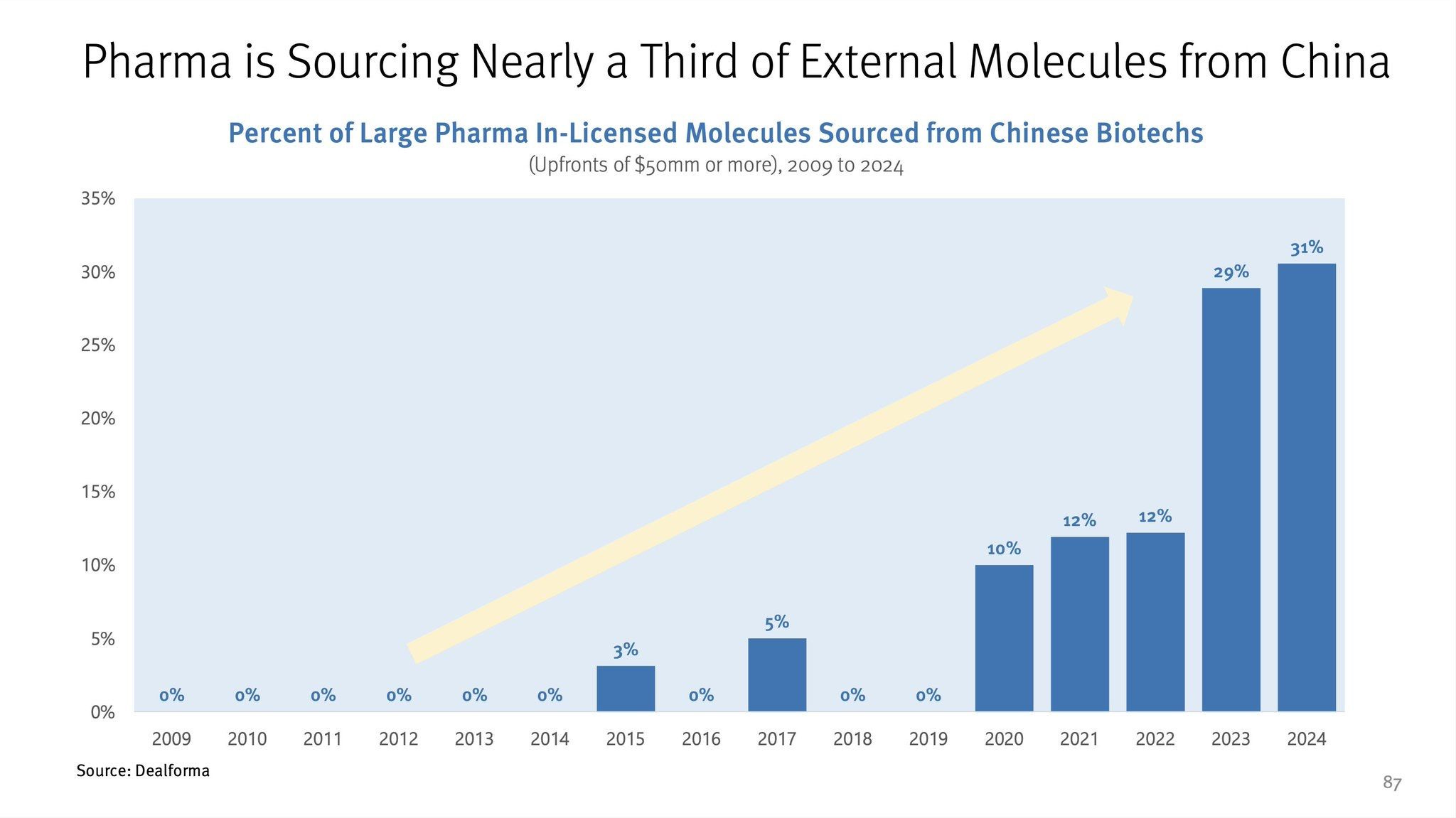

One-Third of Pharma Molecules Now Come from China

Eric Dai, an investor with experience at Andreessen Horowitz’s Bio Fund and currently part of Dimension’s investment team, shared a striking observation from a recent Stifel Bank report: one-third of molecules acquired by major pharmaceutical companies now originate from China, compared to nearly none four years ago.

This rapid shift highlights China’s growing influence in biotech and and may raise concerns about the competitiveness of the U.S. biotech ecosystem in terms of cost, quality, and time-to-market.

Takeaways

China’s biotech sector has transformed into a major global hub, producing assets that are increasingly attractive to big pharma.

Standardized workflows and technologies in early drug development have diminished geography’s role in determining competitive advantage.

Despite heavy investment in U.S.-based biotech, ROI has been questioned as more molecules are sourced externally, particularly from China.

Dai likens this evolution to the outsourcing of industrial manufacturing in the late 20th century, where cost-efficiency and capability drove production to other regions. He suggests that molecular development may follow a similar path, with U.S. biotech facing the risk of becoming less competitive in a globalized marketplace. The growing prominence of Chinese assets highlights advancements in their biotech ecosystem while also raising questions about the U.S. model, where significant venture funding hasn’t always resulted in highly sought-after M&A assets.

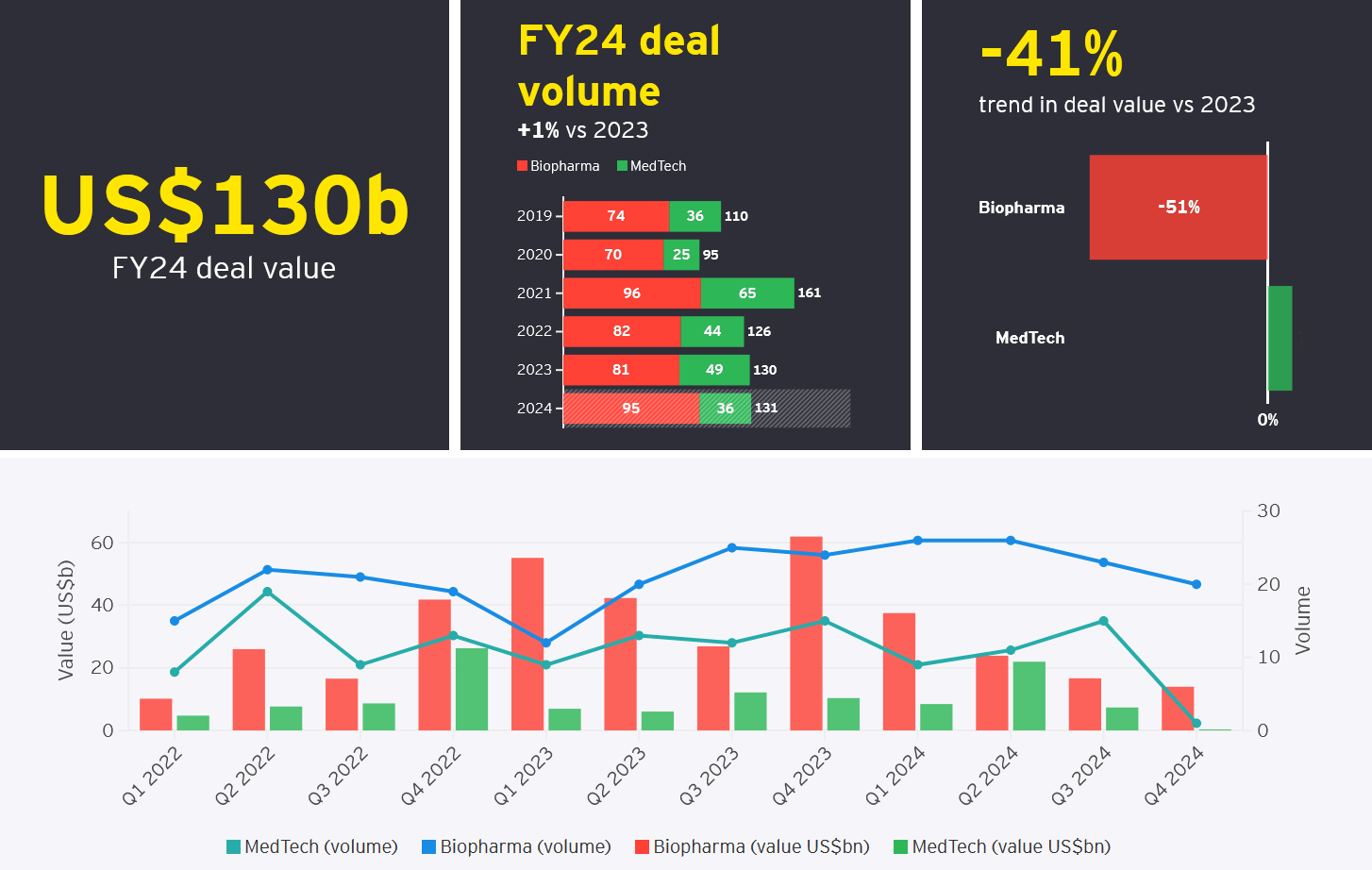

Biopharma M&A: 2025 Outlook

While we’re on the topic of M&A, let’s mention a recent analysis from EY’s Firepower report: life sciences dealmaking – trends in 2025, released with the start of the now ongoing 43rd Annual J.P. Morgan Healthcare Conference.

According to EY, the past year amounted to something of a “reset” for larger mergers and acquisitions, as deal value plummeted despite a steady volume of transactions. In 2024, life sciences companies shifted away from the mega-deals of 2023 to focus on smaller, bolt-on acquisitions and pre-Phase III assets—bids that are, as EY describes them, “smaller, smarter and more agile.” This move allowed buyers to secure promising treatments earlier in development, while hedging costs and risk.

At the heart of this dynamic, EY points to three primary drivers heading into 2025:

Firepower: The top 25 biopharmas still have roughly $1.3 trillion in capital set aside for deals, although it’s unevenly distributed among select giants like Novo Nordisk and Eli Lilly.

Patent expiration: By 2028, expiring patents could strip the industry of $300 billion in revenues, forcing many big players to keep building pipelines through strategic acquisitions.

Policy tailwinds: With a new, business-friendlier U.S. administration taking office, the industry anticipates a more benign regulatory environment and potentially lower corporate tax rates.

On the flipside, EY acknowledges constraints, including still-high valuations for prime targets, fewer de-risked late-stage assets on the market after 2023’s M&A spree, and lingering cost concerns. Another wildcard is the Federal Trade Commission: While the expectation is for a lighter touch in reviewing deals, changes in leadership and priorities can create pockets of uncertainty for buyers and sellers alike.

While M&A has indeed been active, it has mostly involved earlier-stage assets. The cumulative price tag for industry deals shrank by more than 40% from 2023 to 2024, as opposed to the higher-value but fewer-volume deals of previous cycles. EY foresees 2025 as potentially seeing a return to bigger transactions, thanks in part to declining interest rates and greater post-election clarity in the U.S.

EY also highlights the growing importance of AI collaborations and cross-border partnerships, particularly with emerging Chinese biotechs. Across 2019–2024, EY counted 330 AI-focused partnerships or acquisitions, signaling how integral data-driven drug discovery has become. Meanwhile, Chinese biotech innovators, particularly in oncology, have piqued Big Pharma’s interest with novel platforms and therapeutic modalities—though integrating cultural and operational differences remains a challenge.

Despite these promising signs, the immediate picture for early-stage funding remains mixed. As EY points out, venture capital continues to concentrate on companies that have proven management teams or established platforms, leaving newer entrants or riskier technologies scrambling for financing. Nevertheless, EY concludes that M&A—in all shapes and sizes—will remain the cornerstone of future growth, as many leading pharmaceutical companies depend significantly on products acquired through mergers or partnerships.

In short, the smaller “bolt-on” deal trend that took hold in 2024 is likely to continue, but 2025 could well see larger moves once the big players digest recent buys, adapt to reduced borrowing costs, and seek faster fixes for looming patent cliffs. With the easing of macroeconomic and political uncertainty, dealmakers might finally feel ready to put some of their substantial acquisition capital to work.

Read also:

11 Biopharma Trends to Watch in 2024

Very informative